The Fed Presses the Pause II Button

Wednesday, June 14, 2023

Pause II

The Federal Reserve announced today a pause in their historic rate hike campaign. The Fed has increased interest rates at the last ten consecutive meetings in an effort to curb inflation. The inflation rate, as measured by the US Consumer Price Index, pushed above 9.0% late last summer and recently dropped to a more palatable 4.0%. While inflation is still well above the Fed’s long-term target (2.0%), there is a lag associated with inflation falling in response to rate hikes, suggesting the downward trend for inflation should continue even after this pause.

The culmination of the Federal Reserve’s efforts has had notable impacts on the investment market for fixed income. The US yield curve remains inverted with short-term bonds yielding more than longer-term bonds. Current cash yields have reached their highest level in over 15 years.

Following this pause by the Fed, the natural question now is whether they are done raising interest rates, and when can we expect them to begin cutting rates. While no definitive answer exists, the current market sentiment suggests the Fed could consider a rate cut by early next year. Should that transpire, we would anticipate a commensurate and swift decline in the yield on cash.

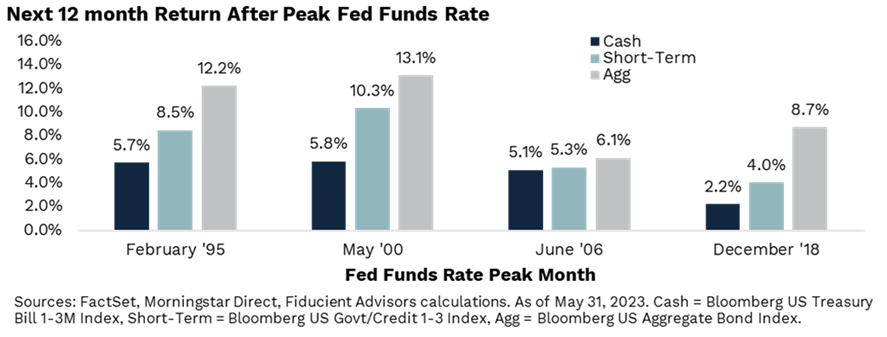

Hold Cash or Invest?

Cash is currently king, but its time atop the mountain may be short-lived. Cash will always have a place in portfolios for investors that have short-term needs where protecting principal is paramount. However, for a more typical investment horizon, cash often proves suboptimal as bonds tend to provide higher total returns over the long-term. In fact, since 1978, the Bloomberg Aggregate Bond Index outperforms cash (as measured by the ICE BofA US 3M T-Bill Index) approximately 67% of the time on a rolling 1-year basis and that figure jumps to 89% if we expand the rolling period to three years.

We do not believe in timing interest rates, but we are likely closer to the end of this interest rate hiking cycle than the beginning. Historically the prospects for traditional fixed income compared to cash when rates peak looks appealing. Following the month of the peak Fed Funds Rate, longer duration fixed income assets have outperformed cash over the following year, often by a wide margin.

As always, please reach out with any questions; we would be happy to discuss our thoughts on these events in further detail with you.

Disclosures

INVESTMENT AND INSURANCE PRODUCTS ARE | NOT FDIC Insured | NOT bank guaranteed | MAY lose value

Riverview Trust Company investments are not insured or guaranteed by the Bank, the Federal Deposit Insurance Corporation or any other government agency. Non-deposit products are subject to investment risks, including possible loss of principal. Past performance does not indicate future results. Asset allocation does not assure or guarantee better performance and cannot eliminate the risk of investment losses.

Riverview Trust Company does not provide tax or legal advice. The information presented here is not specific to any individual's personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances.

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.