Broadening the Rally

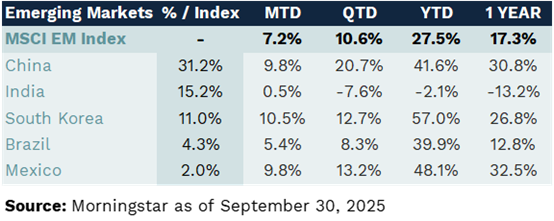

September saw a meaningful expansion in market leadership, with emerging markets and U.S. small-cap equities stepping into the spotlight. The MSCI Emerging Markets Index posted a 7.15% gain for the month, outpacing developed peers and marking its ninth consecutive monthly advance. Strength was concentrated in China, Brazil, Mexico, and South Korea where improving investor sentiment, favorable currency dynamics, and supportive policy environments helped drive returns. The rally was not limited to headline indices—growth-oriented segments within EM led performance, with technology and consumer discretionary sectors delivering outsized gains. This rotation suggests investors are increasingly willing to re-engage with regions that had previously lagged, reflecting a more constructive global risk appetite.

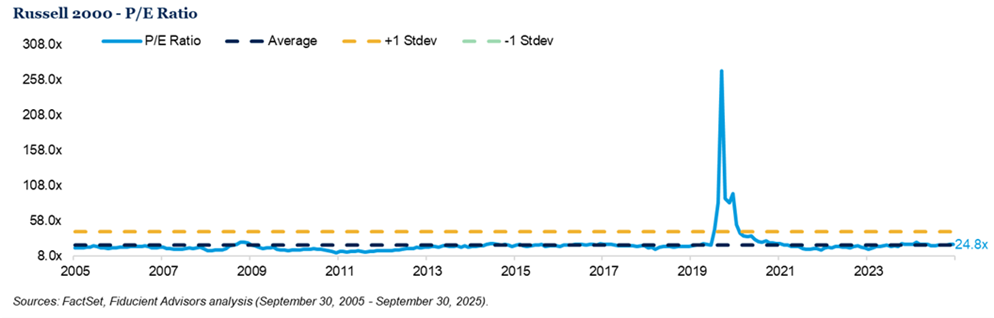

In the U.S., small-cap equities also staged a notable comeback. The Russell 2000 Index rose 3.11% in September, benefiting from the Federal Reserve’s rate cut and a more favorable macro backdrop for domestically focused companies. While large-cap growth has dominated year-to-date performance, the recent strength in small caps points to a broadening of participation and a potential shift in investor preference. Lower borrowing costs, improving labor market dynamics, and resilient consumer demand all contributed to the rebound. Importantly, the rally was accompanied by expanding market breadth and declining volatility, reinforcing the view that equity markets are transitioning from narrow leadership to a more inclusive phase. As of September 30, the Russell 2000 traded at 24.8x (or "times") forward earnings, aligning closely with its long-term average and suggesting valuations remain reasonable despite the recent rally.

Looking Ahead

The macro environment in September provided a supportive backdrop for both emerging markets and U.S. small-cap equities. The Federal Reserve’s rate cut signaled a shift toward more accommodative policy, easing financial conditions and lowering the cost of capital for smaller, domestically focused firms. Simultaneously, improving global liquidity and a softer U.S. dollar helped bolster emerging market assets, particularly in countries with high external debt exposure or export-driven economies. Inflation data remained contained, and labor market indicators pointed to a gradual cooling rather than a sharp slowdown, which helped sustain risk appetite. These dynamics encouraged investors to rotate into areas that had previously lagged, including EM growth sectors and U.S. small caps, reflecting a more constructive view on global economic resilience and the potential for broader participation in the equity rally.

Please reach out with any questions; we would be happy to discuss our thoughts on these events in further detail with you.