Déjà Vu All Over Again

Monday, May 9, 2022

Yikes. Through today, the S&P 500 is down roughly 16.0% year to date. Adding insult to injury, the yield on 10-year Treasuries has risen sharply, from 1.60% at the beginning of the year to above 3.00%, causing bond prices to fall. The US bond market, as measured by the Bloomberg US Aggregate Bond Index, has lost nearly 10.0% year to date, among the worst starts to a calendar-year on record. This simultaneous decline in both stocks and bonds is highly unusual, having happened only a handful of times since the 1970s.

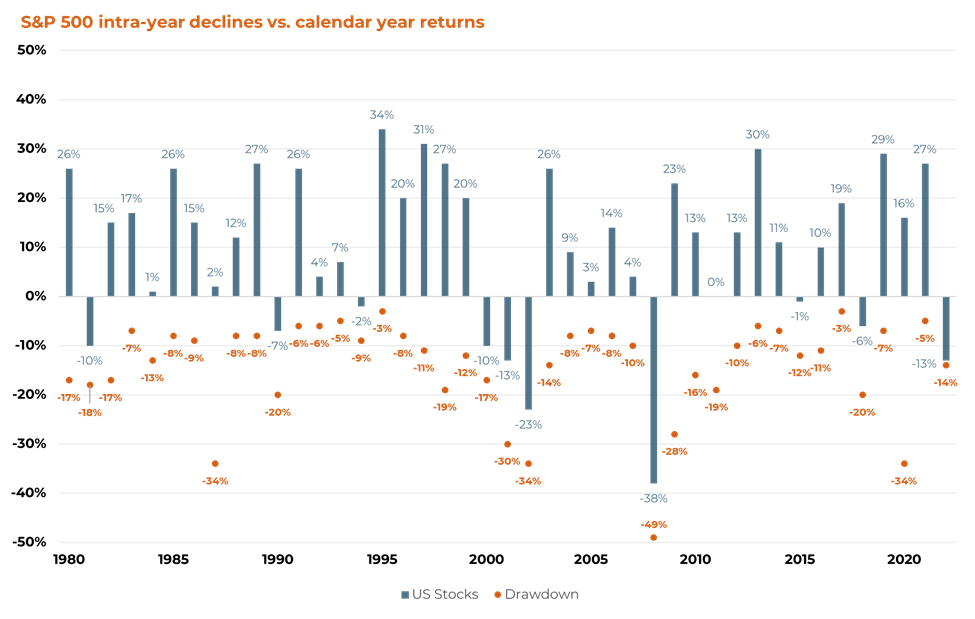

However, if we let history be our guide, research shows that market corrections (a drop in value of 10% or more) happen about once every two years on average for the S&P 500 Index. Such corrections, though unpredictable, are normal, and historically don’t last long. Moreover, despite average intra-year price declines of 14.0%, annual returns for the S&P have been positive in 32 of the last 42 years. Positive results for bonds have been even more common, with only four negative calendar-year results since 1980. In the end, market volatility is as uncomfortable as it is normal, and we must remind ourselves that investment markets are resilient.

If this all sounds familiar, it’s because we’ve written about it several times in the past few years. What we know from weathering these recurring bouts of volatility is that market prices move on fear of future events as much as on facts themselves. Taking inventory of the current situation is often helpful to understand the backdrop and context for what fears might be driving market behavior.

Here are the facts as we know them today:

- Persistent inflationary pressure: The recent 8.5% reading is the highest since December 1981. This is not a US specific issue, as inflation across the European Union has also accelerated by nearly 8.0%. The forces behind the general rise in prices have been building for a while, and it will likely take quite some time to return to “normal” levels.

- Geopolitical concerns on the rise: The Russia/Ukraine war has resulted in a massive humanitarian crisis. Countries are seeking new trade partners in an effort to move away from reliance on Russia, leading to a far more costly and inefficient distribution of resources. The short-term impact of this is higher prices, but the long-term upside is improved national security for these countries.

- Waning economic undercurrent: The US recently posted a negative -1.4% GDP figure as private inventory investment, exports and government spending decline. What this report masks, however, is that household and business capital spending (the largest driver of economic output) remains very healthy.

- Rising interest rates: As expected, the Fed announced a 0.50% hike to their key rate on May 4th. The Fed remains committed to combatting inflation and restoring price stability with future rate hikes on the horizon.

- A burgeoning COVID outbreak in China: Tens of millions of people are under mandatory home confinement. This will likely have a ripple effect on the global supply chain and economic activity.

These observations tell us that the current environment is rocky, and if marketmoving-fears-of-future-events are based on the current situation, the next several months may very well be a bumpy ride. But these circumstances (and others unknown to us now) will interact in ways that cannot be predicted, even though we may be tempted to think that the future is more predictable.

What’s the roadmap?

Diversify and stay disciplined. Diversification, as always, is critical to avoiding the hurt from a big drop in a single portion of your portfolio. Diversify globally in case the dollar weakens and other countries perform better than the U.S. Diversify by size, in case this environment favors smaller companies rather than larger ones. Diversify across style, in case higher interest rates and inflation brings an end to the decade-long dominance of growth stocks over value. And stay disciplined by focusing on your time horizon, which is the most important piece of your investment strategy. Make sure you have enough cash on hand (or existing cash flow) so that you don’t have to sell in a down market. Future market movements are impossible to predict, even in less stressful times than these. But know that we’re taking the ride with you, and we’ve been down this road before.

Disclosures

INVESTMENT AND INSURANCE PRODUCTS ARE | NOT FDIC Insured | NOT bank guaranteed | MAY lose value

Riverview Trust Company investments are not insured or guaranteed by the Bank, the Federal Deposit Insurance Corporation or any other government agency. Non-deposit products are subject to investment risks, including possible loss of principal. Past performance does not indicate future results. Asset allocation does not assure or guarantee better performance and cannot eliminate the risk of investment losses.

Riverview Trust Company does not provide tax or legal advice. The information presented here is not specific to any individual's personal circumstances. To the extent that this material concerns tax matters, it is not intended or written to be used, and cannot be used, by a taxpayer for the purpose of avoiding penalties that may be imposed by law. Each taxpayer should seek independent advice from a tax professional based on his or her individual circumstances.

These materials are provided for general information and educational purposes based upon publicly available information from sources believed to be reliable—we cannot assure the accuracy or completeness of these materials. The information in these materials may change at any time and without notice.